Recently we published the start of our look back at the crisis that paralysed Scottish football. It centred on Risk. Mainly existential risks that exist because ‘success’ is measured in trophies and league positions not pennies and pounds. Or at least historically – the big leagues are now increasingly becoming home to investment portfolio assets.

The full article can be found here. It explains in more detail how club licensing (including UEFA licensing) is ostensibly there to help make sure clubs are run sustainably and without gambling on success, but isn’t actually fit for that purpose.

This follow up was prompted by two sets of figures being released recently – those of Dundee and Rangers – which brought the issue of risk and safeguards against failure starkly back into focus.

Dundee

The Dundee accounts can be found here. They paint a picture of a club that is Balance Sheet insolvent (liabilities exceed assets) and posting unsustainable losses. Post year end the position will improve, but it’s due to a debt for equity swap, where a major shareholder converts part of it loan (reducing liabilities) in exchange for shares. This does not provide cash to keep funding the losses. Fresh injections of cash will as the loans are already spent.

Dundee are now an established top tier club. They’ve been rocked by financial catastrophe twice already. They supposedly set strict Key Performance Indicators to prevent it happening again. Yet look where they are… running wages to turnover ratios way higher than the league average (78% while 60% viewed as healthy) and posting successive losses.

Dundee look every bit a club staring at the abyss again.

Rangers

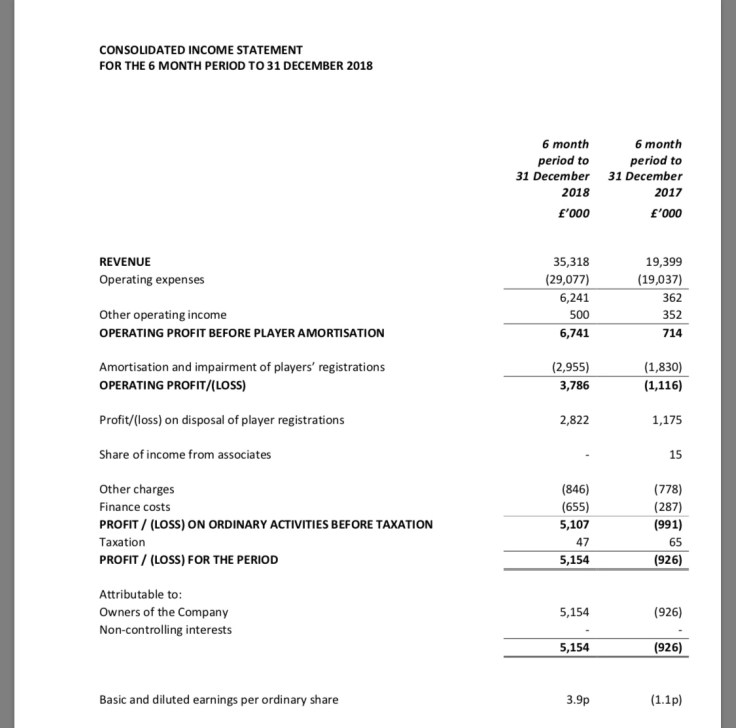

Rangers also released a set of performance figures. They aren’t really accounts being as it’s only their “trading results” – a Profit and Loss Account. They show a notable upturn to the comparative period. They don’t contain all the things you’d expect to see in a proper set of interim financial statements though. By that I mean a set prepared under IAS 34 or local accounting standard equivalents. They didn’t contain for example a Balance Sheet, last annual period comparatives or Notes to the Financial Statements. They also did not contain a report from the auditors covering their review of the interim results (conducted under ISRE 2410). That doesn’t really matter a jot to Rangers as, having been delisted, they are not required to publish such a full set of interims.

It raises the question though, why did they publish this then? Wanting to publicise the upturn in performance is one possible reason, though Rangers did similar with last years numbers. It also doesn’t explain why (I’ll get to why cost not a factor) they wouldn’t just publish a full set of interims, instead of cherry-picking what went out.

A possible reason subsequently came to light when a floating charge was registered in favour of Close at Companies House shortly after the trading performance was release. Now, there is nothing wrong with utilising borrowing to smooth out cash flow. It does come at a cost though of comparatively high interest rates and big penalties for default. Those costs are reimbursement for the lender for their risk in loaning. They are worth looking at for that reason – an indicator of how the market perceives risk at that company.

There’s not much info on the loan interest itself in the annual accounts (repaid last Close loan) or interim release (disclosure limited). You can look at the numbers though.

That ‘finance cost’ of £655K is up a lot on the comparative. The “other charges” is basically an accounting treatment to recognise a notional interest rate on interest free loans from directors so it’s nothing to be immediately concerned with other than to give an idea how much similar borrowing might cost that wasn’t on such terms. It could be withdrawn.

That ‘finance cost’ of £655K is up a lot on the comparative. The “other charges” is basically an accounting treatment to recognise a notional interest rate on interest free loans from directors so it’s nothing to be immediately concerned with other than to give an idea how much similar borrowing might cost that wasn’t on such terms. It could be withdrawn.

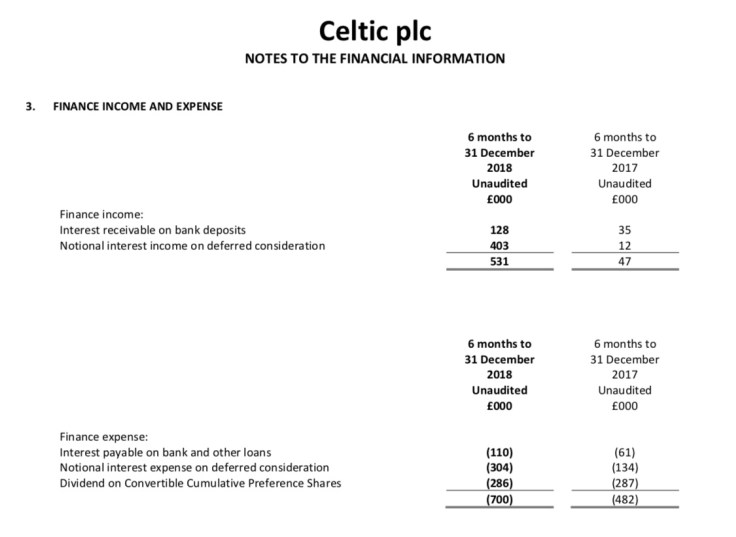

A relevant benchmark might be comparable clubs. The closest fit would be Celtic.  The notional interest here is a similar item to that described in the Rangers accounts as other charges. The preference share dividend is Dermot Desmond’s return on investment for his alternate share class. It’s really therefore the £110K we are comparing it too. Within that framework it’s clear Rangers are paying about six times as much as Celtic to fund borrowing requirements with significantly less turnover.

The notional interest here is a similar item to that described in the Rangers accounts as other charges. The preference share dividend is Dermot Desmond’s return on investment for his alternate share class. It’s really therefore the £110K we are comparing it too. Within that framework it’s clear Rangers are paying about six times as much as Celtic to fund borrowing requirements with significantly less turnover.

None of this however is a problem so long as it’s sustainable long term. Perhaps it is, but the more relevant point is that the SFA would be blissfully unaware if it wasn’t.

As we discussed in that earlier article, the financial information looked at for domestic licensing purposes is so low to be irrelevant. Mainly, if your auditors issue a going concern warning you need a good explanation. Nothing about breaking even over time etc.

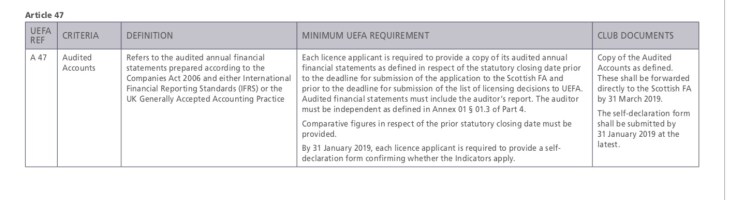

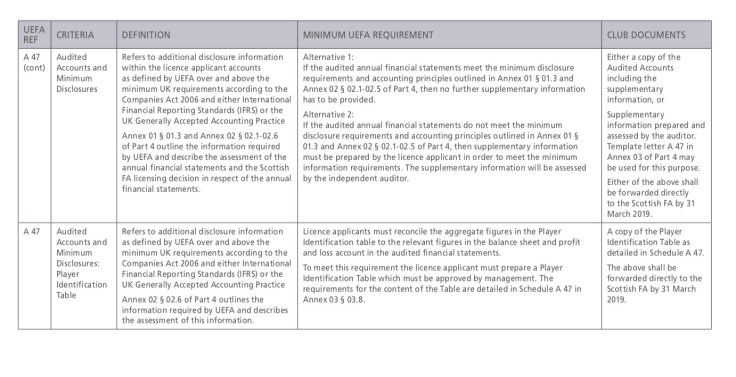

Relevant to this discussion however is the UEFA licensing requirements. Here’s the relevant bits relating to financial statements:

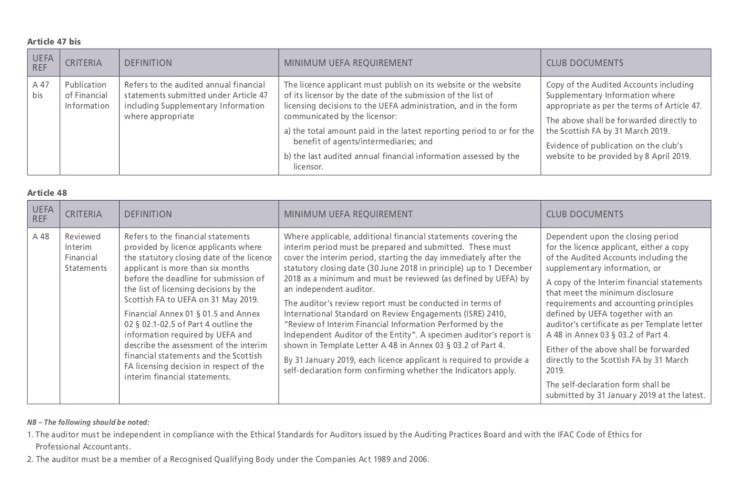

The really relevant part is the last one, Article 48. It requires the applicant to submit a proper set of interim accounts (assuming a June year end) to December that is in accordance with accounting standards and has had an Auditor’s Review done and report given. This isn’t a full audit but provides some comfort that the accounts are not misleading based on a limited amount of work done by the auditors.

The really relevant part is the last one, Article 48. It requires the applicant to submit a proper set of interim accounts (assuming a June year end) to December that is in accordance with accounting standards and has had an Auditor’s Review done and report given. This isn’t a full audit but provides some comfort that the accounts are not misleading based on a limited amount of work done by the auditors.

Rangers will therefore be preparing a full set of interims and getting them reviewed. They will be submitted for licensing, but they don’t need to be made public. So they haven’t. That’s not odd. Releasing something else instead is strange though. Cost is clearly not relevant since it needs to be done anyway and would actually be marginally cheaper to only prepare one set rather than two (the published version being highly abridged).

Domestic FFP

The two situations above themselves do not give any real conclusions as to whether a plan is in place and that plan is sustainable. They only raise questions. We can be relatively certain the SFA will receive the Rangers proper interims and will rightly keep them confidential. That doesn’t contain a business plan.

It would settle a lot of nerves to know that the SFA – or indeed the SPFL should authority be devolved – were actively monitoring financial health on an ongoing basis for both those who appear at high risk of failure (Dundee) and those on which a failure would be catastrophic (Rangers). A risk based approach to regulation and monitoring in other words.

Not so long ago Better Capital (a venture capital fund) was roundly criticised when City Link employees found out the company was to collapse at Christmas. What made the rounds in auditing circles on the back of that was that the accounts past the going concern tests on the strength of support from the fund that it intended to provide sufficient funding to meet the company’s expenses for the foreseeable future. They pulled the support months later. When asked about that promise of support, it was reported that it was their intention at the time, now it is not.

By a strange coincidence the man behind that fund, Jon Moulton, is also the chairman of the company that acted for David King in confirming the cash in escrow ahead of the recent share purchase offer.

The reason for bringing this up however is that both Dundee and Rangers have expressed a need for further outside finance to continue as a going concern. It appears promises have been made. These days decent auditors tend to consider such promises as only having value when legally enforceable. Both Dundee and Rangers have small audit firms auditing them who may well be unaware of such issues. One would certainly hope the SFA as regulator holds its own standards rather than relying on others. Being reliant on funding sources that cannot be reasonably certain of materialising sails very close to the wind.

Additionally the auditors would typically only consider the “foreseeable future”, ordinarily defined as within one year of signing their report. That focus on immediate issues means their work is never intended to be an opinion on longer term sustainability as the SFA seems to take it within their licensing procedures.

One would think their fans and fans of all Scottish football teams would breathe a lot easier knowing their future was safe and under scrutiny meaning they would know should things look troublesome.