Thought it was easier to set something out here than speaking with lots of different people about what today’s story in The Times is really all about. Its already become a bit of a raging argument on Twitter between Rangers fans feeling upset about the course things followed and Celtic fans making light of it, so thought I’d set out where I think the real crux areas of it are here given the limitations of Twitter as a medium for explanation. No surprises its somewhere in the middle – between revision of history and the headline numbers banded around when Rangers sank in 2012. More in hope than expectation that some of the more outrageous takes on it all can be grounded in sense.

There’s a number of issues within but none of them are really as clear cut as the sensationalist headlines would suggest. None of them are actually all that new either. There’s three real issues relating to the total figure within that need to be considered both together and seperately:

- The calculation error;

- The calculation method; and

- The penalties.

1. The Calculation Error

The report says that HMRC acknowledged that it had claimed for too much. The article itself picks this item up:

“A further £2m has also gone after certain parts were agreed to have been overstated and there may be a further reduction in the pipeline”

It does then get sensationalised a bit to make it sound as though this is the root cause of all Rangers woes;

“Up to £50 million is set ot be wiped off the tax bill owed by the Ibrox club’s old operating company after HM Revenue & Customs acknowledged it had claimed for too much”

As noted the error acknowledged was only £2m. A further £24m the Times explains as relating to penalties (see item 3) rather than the tax bill itself. There doesn’t seem to be any suggestion of error relating to that. The remaining £24 million not accounted for in the £50m figure only really gets a vague referencing:

“…and there may be a further reduction in the pipeline”

I believe, and this bit is a little conjecture on my part, that the issues discussed in item 2 are the items referred to. The basis for this is that it is a known issue relating to the tax computation that had remained unresolved even following the Upper Tax Tribunal decision. It was also known about back in 2011 too as a matter yet to be resolved rather than as some later undiscovered error which does beg a few questions of why it is being presented this way.

2. The Calculation Method

The article explains:

“The tax authorities had pursued the main EBT tax liability as a gross figure rather than just for the tax that should have been paid on it. It is thought that if HMRC was to just look at a net figure sum for the EBT liability , then the final bill would drop closer to £20 million”

This issue was one of what the monies actually paid out to the footballers and others represented. I’ve explained it a wee bit on twitter already in simple terms so I’ll just pop that up as a rough and easy to follow explanation.

Just shy of £50m in payments went through the Remuneration Trust into individual EBT’s and the tax that HMRC was chasing was based on the second model (which ignores NIC for ease of explanation) which would obviously give a higher figure for the tax due. The UTT of course didn’t deal with the quantification of the amount due, only its nature – which it concluded was unlawful avoidance of PAYE and NIC.

In January 2011 the issue of “Grossing Up” had become part of the dispute between HMRC and Rangers. It would never be resolved, though there is every chance HMRC will drop chasing it now given – whether right or wrong – its largely now irrelevant to any potential recovery. Just good money after bad from the public purse.

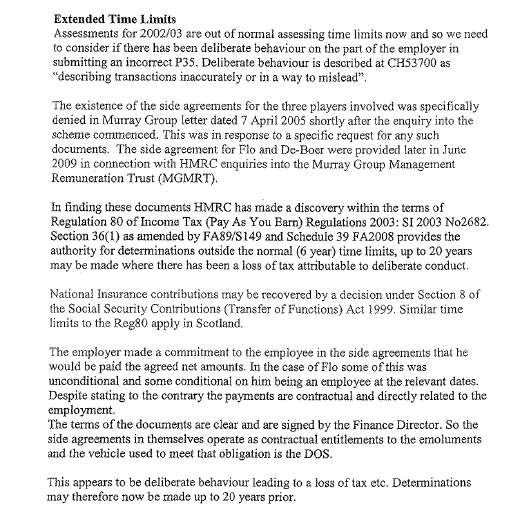

A letter from HMRC to Mr McGill of Rangers dated 23 February 2011 explains how the issues of misleading HMRC had been viewed and why the normal 6 year time limits wouldn’t apply.

An important part of this letter (though it actually relates to the DOS rather than EBT liability) is that the letters indicated the payments were to be net due to how the agreements worked. It wouldnt be so clear cut in the later EBT cases. There is a reasonable case to be made that Rangers could have won that particular argument and got the lower amount, but the more important thing to note is that it was only ever part of an ongoing discussion at the key time about exactly how much was owed. The fact that any was owed had yet to be definitively established before putting a number on it.

A new owner coming in around the time that Whyte did may have been able to convince HMRC – if clearly intending to make good on historic issues they were inheriting – to go for the least financially punitive method as part of a structured repayment plan. That would have involved accepting liability however. I’d imagine (given no real benefit now to HMRC in pursuing and liquidators may well see it as worth pursuing) that this concession may also be later made to the remaining liquidation creditors whether it has grounds or not. For the avoidance of doubt, I think Rangers may have been able to win on this one, but their Directors actions burned up any goodwill HMRC may have shown them.

3. The Penalties

“.. a £24m penalty charge has been wiped out”

To understand the penalties issue it is necessary to reflect on why it was being pursued and why it is now being dropped.

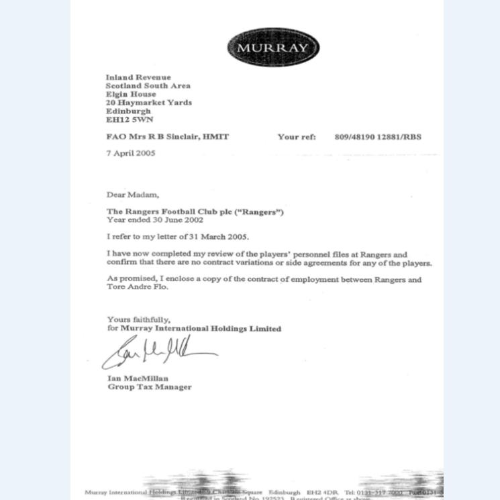

HMRC had found it difficult to reach a determination on whether Rangers use of EBT’s ought to have been taxable because important information was not only being withheld but obfuscated. As far back as 2004 Rangers had been denying the presence of letters detailing the amounts to be paid through the EBT’s and avoiding the questions of how the amounts were calculated.

This resulted in something of an impasse in the HMRC investigation between 2004 and 2007. During this time it would also appear that Rangers mislead their auditors (Grant Thornton) as to the nature of the payments and the dialgoue with HMRC.

As a result of the impasse through correspondence, HMRC on 21 September 2007 made a request for all documentation relating to Trusts 13, 38 and 63 (McCann, Arteta and Boumsong). The information provided by Rangers again omitted the side letters, though unknown to them, HMRC in October 2007 had been provided with them from the evidence passed following the July police raid. This despite Rangers insisting all through the period that no such letters existed.

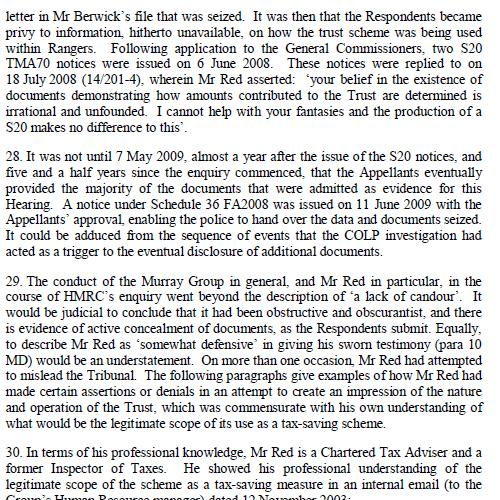

Unsurprisingly this led to follow up questions from HMRC on the existence of side letters long denied. ‘Mr Red’ , believed to be Ian McMillan once again, replied to the s20 notices as follows:

“your belief 5 in the existence of documents demonstrating how amounts contributed to the Trust are determined is irrational and unfounded. I cannot help with your fantasies and the production of a S20 makes no difference to this”

HMRC would go on to call Mr Red’s behaviour “obstructive and obscurantist” and describe evidence of active concealment of documents.

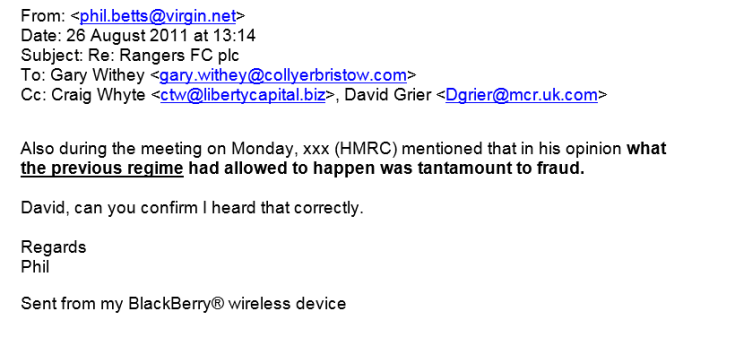

The end result of this period of time would see HMRC send through demands relating to the EBT liability or “Big Tax Case” in 2010 which Rangers would appeal. HMRC would ultimately tell Rangers that they considered the behaviour ‘tantamount to fraud’ which gives a pretty strong indication that they felt penalties were appropriate.

It was put to me on Twitter that HMRC would not just drop the penalties if there was not some reason to do so. There is 2 very good reasons to do so:

i) They have not yet established their rights to receive payment for those penalties (or indeed final quantum on the means of calculation which might follow this same rationale in end outcome); and

ii) It will cost them (and therefore the public purse) more money to pursue it than they are ever likely to receive in recovery.

There is a decent argument to be made that Rangers were disadvantaged in negotiating position by HMRC’s desire to get a high profile scalp and legal prededent set on EBT use. The same argument doesn’t really apply to either the quantum or the penalties since neither ever were argued in court.

Normally on a takeover HMRC would give the new owners decent terms on historic issues, but it’d be up for discussion as the deal progressed. The case that did go through may have had a bit of an impact there, but it really seems unlikely that a theoretical argument about the final figures would have been a deal killer if someone had got to that point of a takeover deal.

On the issue of penalties, even the DOS penalties were still not finalised at the time of Whyte’s takeover. It’s also of course relevant to say that while HMRC accepted BDO’s appeal against the scale of the penalties (65% is high – but I’ve explained why it was so high) it hadn’t decided they were wrong altogether. Given the beneficiaries of liquidation proceeds now are the creditors, not the old Board against whom the high rate was applied, they appear to have elected to remove the penalties altogether as of October 2018. Good news you would think for the remaining creditors, but not part of a mistake. Certainly not £24m worth of mistakes. This element may very well have been negotiable by a prospective new owner around the time Whyte arrived on the scene, but it is extremely unlikely they’d have got as good a deal as HMRC have given the remaining liquidation creditors.

Interest in the club

Andrew Ellis made his interest known in May 2010 – a few weeks after Rangers April 2010 announcement that they were under investigation re their use of EBT’s. It would collapse in June that year when David Murray announces publicly the club is no longer for sale.

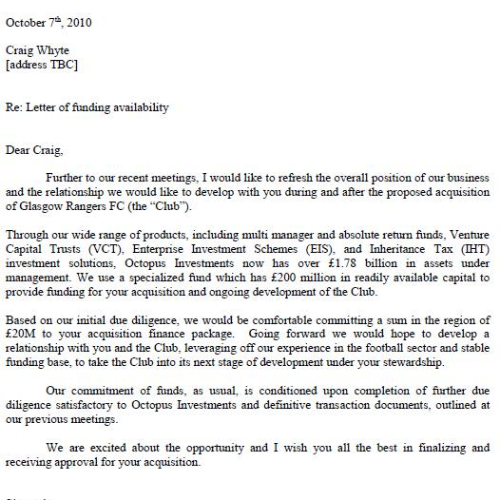

By October 2010 Craig Whyte was working on his takeover of Rangers and Octopus/Ticketus would bank roll it.

On 6 May 2011 the Share Purchase Agreement with Craig Whyte’s Wavetower was entered into. In between times the ‘Grossing up’ issue had reared its head in February 2011 (see Item 2) in relation to the DOS scheme which was at a more advanced stage than the EBT liabilities.

“At the time of the sale of the club in 2011, had the tax claim been at the level now being reported then, in my opinion, the outcome would certainly have been a much higher level of interest in acquiring it and therefore more potential buyers”

John McClelland, former Rangers Chairman

It seems a little fanciful to think it would have made any real difference to the prospects of a sale at the time given there was only one active takeover being pursued by the time the grossing up issue reared its head. This issue alone does account for very large chunk of the amounts being pursued that are later quantified, but even the liability at this point hasn’t been confirmed (it is still going through the court processes) never mind the quantum. Meanwhile Lloyds are frantically trying to get out any way they can and pressuring David Murray to sell. By March 2011 the Board and Lloyds were already making contingency plans for a liquidation event.

So in short, it might have made a few potential investors change their mind a bit about the level of liabilities back in 2011 needed to keep Rangers as a going concern, but by this point things were looking grim anyway. Its also not very clear that there were other investors willing to come in. Anyone that did would have been given access to the data room and able to see the potential scale including the issue of gross v net that would need to be seperately resolved one way or the other.

For this argument to really have legs it kind of needs to be looked at as:

“Why didn’t HMRC immediately concede that the amount of tax due was the lower threshold and that it never had any real prospect of collecting penalties”

No one ever gives up their negotiating position in this way even if settlement is made, and anyone seriously looking at buying Rangers would have known some negotiation was possible – especially for a new owner.

The total quantum lodged with the liquidators BDO by HMRC was £94m (much of which was still not finalised including penalties and ultimate quantum of the EBT liability).

Of this £74m related to the EBT scheme in total with the other £20m the DOS scheme liability plus an awful lot of unpaid PAYE, VAT and NIC under Craig Whyte’s regime. Its important to remember though that Whyte’s non-payments actually just extended the time until Rangers went into Administration while he wheeled and dealed trying to hit a home run through European runs and player sales. Realistically a good negotiator might have been able to shave £30m off that if recovery was possible.

So – why now?

This information has been in the public domain for or quite a while (since December 2018, almost a year, then also included in the June 2019 report), but it has never been given this spin and polish.

It does beg the question ‘why now?’.

It may be the fact (though I think it unlikely) that its an intended distraction from the court case with Memorial Walls or the ongoing issues with Sports Direct. A more plausible reason in my own – very personal – opinion is that it is the ground work being laid for the fund raising that Rangers now need to keep their on the pitch efforts at the same level they currently are.

There’s a real chance I’m not correct on this conjecture about the reasons its hitting the news now, but its getting to a point of either scale back or re-tool.